The European Shipper's TMS Marketplace Integration Strategy: How to Build Capacity-Resilient Procurement That Thrives During 2026's Perfect Storm of Driver Shortages and Vendor Consolidation

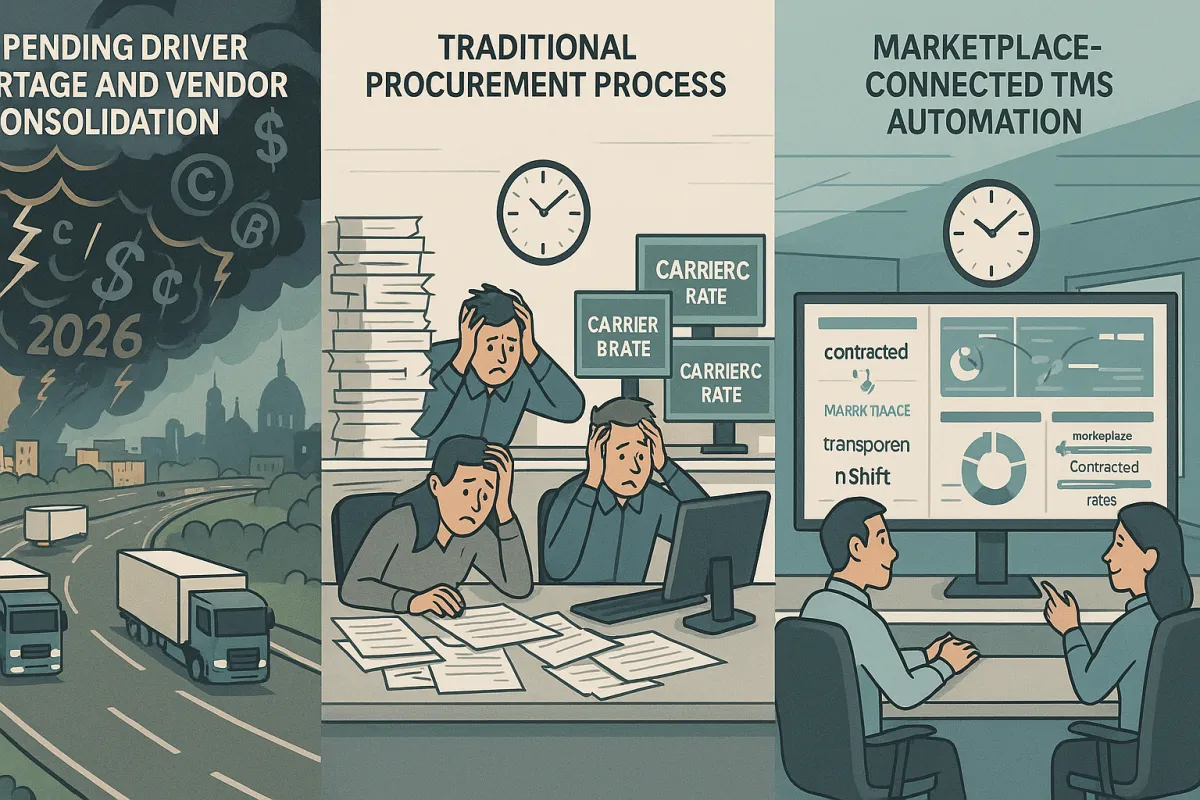

The 2026 Perfect Storm: Why Traditional TMS Procurement Is Failing

Europe could lack over two million drivers by 2026, impacting half of all freight movements, while simultaneously facing the most significant vendor consolidation wave in TMS market history. WiseTech Global's $2.1 billion acquisition of E2open and Descartes Systems Group's acquisition of 3GTMS for USD 115 million signal the most significant vendor consolidation wave in TMS market history. Your procurement window is shrinking faster than available capacity.

The numbers paint a grim picture. Industry reporting points to 426,000 unfilled truck driver jobs in Europe, with data from industry organizations, including the International Road Transport Union (IRU), pointing to a shortage of around 500,000 professional drivers in Europe. Traditional European freight procurement consuming 18-28 hours per tender faces extinction when market capacity simply doesn't exist.

Major TMS vendors are simultaneously disappearing through acquisitions. Beyond WiseTech and Descartes, Körber's transformation of MercuryGate into Infios following their 2024 acquisition represent just the beginning of a fundamental market restructuring. Modern platforms like Cargoson, Transporeon, nShift, and Manhattan Active are addressing these challenges with marketplace connectivity that compresses traditional procurement cycles from days to minutes.

Marketplace Integration vs. Traditional Carrier Networks: What's Actually Different

True marketplace integration isn't about portal access or batch rate uploads. True integration means your dispatcher sees marketplace rates alongside contracted rates in the same tendering interface, with automatic booking and tracking updates flowing back to your primary TMS dashboard.

The workflow transformation is dramatic. Traditional European freight procurement follows a familiar pattern: RFQ creation (2-3 hours), carrier outreach (4-6 hours), quote compilation (2-4 hours), negotiation cycles (8-12 hours), and contract finalization (2-3 hours). Total cycle time: 18-28 hours for a single lane tender.

Marketplace-connected TMS automation delivers measurable gains. Load posting drops from 3 hours to 10 minutes. Rate comparison happens automatically instead of requiring 4-6 hours of phone calls. One German automotive supplier reduced tender cycle time from 72 hours to 8 hours through marketplace connectivity—roughly 89% time reduction.

TMS marketplace integration offers a direct response to these capacity constraints by connecting your existing transport management system to networks of 300+ verified carriers through automated APIs that handle everything from rate comparison to booking execution. Platforms like FreightPOP, Blue Yonder, Oracle TM, and Cargoson are building native marketplace connectivity that provides access to verified carrier networks while maintaining compliance with European regulations.

The Vendor Consolidation Risk Assessment Framework

Your procurement window extends through Q1 2026 before vendor options disappear entirely. WiseTech Global's $2.1 billion acquisition of E2open, expected to complete in 1H26, alongside Descartes Systems Group's $115 million acquisition of 3GTMS in March 2025, represents the most significant TMS vendor consolidation wave in over a decade. Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams.

Acquisition-resistant contracts require specific protections. Contract protection becomes essential during consolidation periods. Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights. Include specific clauses requiring 12-18 months advance notice of ownership changes, with automatic contract review rights triggered by acquisition announcements. Price protection clauses should lock pricing for 24 months following ownership changes.

The current vendor landscape divides into three distinct categories: global mega-vendors (Oracle TM, SAP TM, E2open/WiseTech), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that focus specifically on cross-border European operations. Independent European options provide stability during consolidation periods while maintaining development focus on regional requirements.

Regulatory Compliance as Procurement Leverage

As of January 2026: eFTI platforms and service providers can start preparing for operations. Member States authorities may start accepting data stored on certified eFTI platforms for inspection. From 9 July 2027, all national authorities will be obliged to accept freight documentation in electronic form via certified eFTI platforms.

This timeline creates negotiation leverage that savvy procurement teams can exploit. Use this preparation period to evaluate which vendors demonstrate genuine European commitment versus global platforms treating compliance as an afterthought. Vendors demonstrating integrated CBAM compliance and eFTI readiness reveal their commitment to European markets.

Additional regulatory convergence intensifies pressure in 2026. From July 1, 2026, vans weighing 2.5-3.5 tons performing international transport of goods will be subject to the obligation to use second-generation smart tachographs (G2V2). Simultaneously, as of 1 January 2026, the transitional phase of the Carbon Border Adjustment Mechanism (CBAM) has ended and the definitive phase has begun.

European-focused platforms like Cargoson alongside regional specialists Alpega and nShift typically provide better understanding of cross-border complexity than global vendors that spread development resources across multiple geographic priorities.

Building Future-Proof Marketplace Integration Architecture

The evolution from predictive AI to agentic AI platforms represents the next transformation wave. By December 2026, every serious organization will be running at least one agentic 'factory' directly tied to revenue growth or risk reduction. Modern platforms are building autonomous decision-making capabilities that will execute freight procurement decisions without human intervention.

European telematics market expansion supports this transformation. The number of active telematics devices in Europe is expected to reach 49.77 million by 2026 – growth that reflects not a trend but a structural shift. This data explosion creates integration complexity that marketplace-connected platforms can manage more effectively than point-to-point carrier connections.

Carrier API modernization adds urgency to platform selection. FedEx Web Services (SOAP) will be retired on June 1, 2026. To avoid disruption, please plan to migrate your solution immediately. USPS is switching off the last of its Web Tools APIs (Version 3) in January 2026. All merchants and solution providers should migrate integrations to the new USPS APIs by this date.

Modern platforms like Cargoson, nShift, and Shiptify that build native integrations handle these transitions automatically, while companies managing direct carrier connections face expensive custom development projects during the exact period when vendor consolidation limits procurement options.

Implementation Strategy: 90-Day Action Plan

Days 1-30: Conduct immediate vendor risk assessment. The vendor evaluation criteria must account for European regulatory expertise. Platforms like Cargoson, Manhattan Active, MercuryGate, and Descartes each bring different approaches to ICS2 compliance, but European-native solutions often provide better understanding of cross-border complexity and multi-country regulatory variations.

Days 31-60: Launch marketplace integration pilot programs. The traditional European freight procurement process consuming 18-28 hours per tender can now be compressed to 45 minutes through marketplace-connected TMS automation. This isn't just theoretical efficiency—real European manufacturers are documenting these gains while navigating the worst capacity crisis in decades.

Days 61-90: Execute change management for procurement team workflow transitions. Expect realistic adaptation periods - most teams achieve 60% time savings after initial learning curves. The automated rate comparison alone saved 15 hours per week across their transport team. When you scale this across procurement cycles, the productivity gains compound rapidly.

Focus pilot testing on specific corridors rather than attempting full-scale transformation immediately. European operations typically involve complex master data relationships and varied carrier connectivity protocols that require careful validation before broader deployment.

Cost-Benefit Analysis and ROI Expectations

Quantifying procurement time savings provides clear ROI justification. Across the board, the savings to the shipper averages 20%. Automation using the Banyan solution reduced emails by 90% and saved the shipper at least 800 hours per year in administrative and accounting time. Through its auto load tendering function, LIVE Connect helped reduce Trinity's dispatch time by 90% to only half a second, rather than minutes. Also, gathering quotes previously took 10-15 minutes by phone or email, now it takes just one minute total to pull and view all carrier rates.

Hidden costs during vendor consolidation periods multiply these benefits. Hidden costs in TMS procurement consistently add 25-30% more than initial estimates, turning what looked like smart investments into budget disasters. Plan for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection.

Long-term strategic advantages extend beyond immediate cost savings. The capacity crisis isn't temporary—building procurement efficiency and carrier access now positions your operations for sustained competitive advantage as market conditions tighten further. Modern marketplace integration provides resilience against both capacity constraints and vendor consolidation risks that traditional procurement strategies cannot match.

Compare vendor approaches carefully across pricing models and European expertise. Cost ranges vary significantly, with cloud TMS pricing ranges from $1.00 to $4.00 per freight load booked in the system, while licensed options demand significant upfront investment plus ongoing maintenance fees. For many European shippers, this translates to predictable monthly costs that scale with business growth rather than fixed infrastructure investments. Cloud TMS implementations often conclude within eight weeks, compared to 6-18 months for traditional systems.

Include cost comparisons across vendor types including Cargoson, but prioritize total cost of ownership over initial pricing. European shippers who implement marketplace integration strategies before vendor options disappear position themselves to navigate 2026's perfect storm successfully while competitors struggle with capacity constraints and budget overruns.