The €50,000 Carrier API Integration Trap: How European Shippers Can Build Cost-Effective Migration Strategies Before FedEx SOAP Retirement and TMS Vendor Consolidation Eliminate Budget-Friendly Options

European shippers watching their carrier integration budgets in 2026 face a grim mathematical reality. FedEx SOAP endpoints retire on June 1, 2026, while basic API integrations cost €5,000-€15,000, while complex ERP connections exceed €50,000. Yet here's what procurement teams discover too late: budget overruns hit 75% of European TMS implementations, and 66% of technology projects end in partial or total failure.

The perfect storm brewing isn't just another technical migration. By February 3rd, 73% of integration teams reported production authentication failures after UPS's OAuth 2.0 migration in 2025. Now multiply that failure rate across simultaneous USPS and FedEx migrations while European regulatory deadlines eliminate your flexibility.

The Hidden Cost Categories Most Procurement Teams Miss

That €15,000 "basic integration" quote your vendor provided? It covers one carrier in one country under perfect conditions. European reality demands more. A basic domestic shipper requires 10-15 integrations minimum, potentially totaling 1,000-1,500 hours of labor. For shippers with freight spend exceeding $250M annually, implementation can cost 2-3 times the subscription fee.

The arithmetic becomes brutal when you factor in European complexity. Cross-border operations require support for multiple tachograph systems, varying customs documentation formats, and country-specific reporting requirements. Each integration touches different carrier APIs, authentication systems, and data formats. When DHL Germany operates different requirements than DHL France, your "simple" integration multiplies.

Third-party application integration adds another cost layer. Shippers pay additional fees to integrate with third-party applications, such as SMC license or PC Miler license fees. These costs compound during capacity shortages when you need rapid access to additional routing, rating, or carrier qualification tools.

Most dangerous are the legacy ERP integration bills. European manufacturers discover their existing systems can't handle modern carrier API requirements without substantial customization. What starts as API connectivity becomes ERP modernization, WMS integration, and database restructuring - driving costs past €500,000 for complex implementations.

The 2026 Perfect Storm: API Retirement + Vendor Consolidation

While you're debugging OAuth flows, the vendor landscape is consolidating around you. WiseTech's acquisition of e2open for $3.30 per share in cash equating to an enterprise value of $2.1 billion marks the largest TMS industry acquisition to date, while Descartes Systems Group has acquired Columbus, Ohio-based 3Gtms for $115 million USD in cash.

The procurement window for securing optimal TMS platforms before vendor consolidation eliminates choices and capacity shortages worsen cost structures runs through Q1 2026. Miss this window, and you're negotiating with fewer options while regulatory pressure mounts.

The consolidation creates operational risks beyond procurement. Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams, directly impacting service delivery quality during critical regulatory implementation periods. When vendor acquisitions happen mid-implementation, your project timeline extends while support resources get redistributed.

European shippers face additional pressure from regulatory convergence. As of January 2026: eFTI platforms and service providers can start preparing for operations. As of 9 July 2027: The eFTI Regulation will apply in full. Member State authorities must accept information shared electronically by operators via certified eFTI platforms. Your integration strategy must account for these mandatory deadlines while vendor options shrink.

Strategic Framework: Building Migration-Resistant Integration Architecture

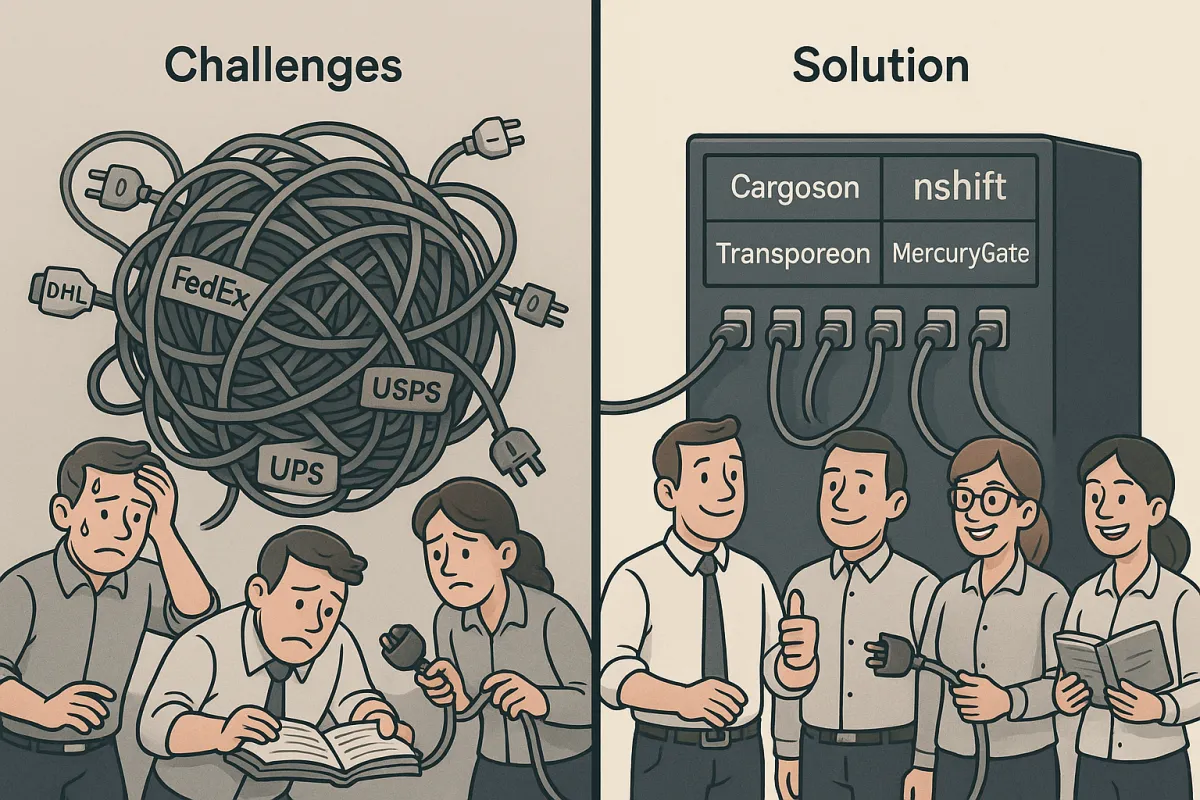

The carriers forcing these migrations won't be your last API headache. Even after these migrations are complete, carriers will continue updating pricing logic, delivery data, security requirements, and services. Smart shippers are building abstraction layers that survive the next round of carrier changes.

API-first platforms from Cargoson, nShift, Transporeon, and MercuryGate provide this protection. Rather than building point-to-point integrations with each carrier, these platforms maintain the carrier connections while exposing standardized APIs to your internal systems. Cargoson, along with competitors like MercuryGate and BluJay, built abstraction layers that handle the OAuth complexity, implement intelligent rate limiting queues, and provide fallback mechanisms when USPS quotas are exceeded.

For maritime integrations, DCSA standards adoption creates similar protection against proprietary carrier systems. European shippers connecting to major container lines benefit from standardized data formats that reduce integration complexity across multiple maritime carriers. The DCSA Track & Trace standard, for example, eliminates the need for separate integrations with Maersk, MSC, and CMA CGM systems.

European regulatory requirements add another layer of integration complexity. Carriers and importers must integrate ERP and TMS systems with the ICS2 platform, with failure to report potentially resulting in a fine of up to 5,000 euros, especially with a large volume of shipments. This means your integration architecture must handle customs data flows alongside carrier connectivity.

The €50,000+ Prevention Playbook: Phased Implementation Strategy

Reactive migrations cost 3-4x more than proactive ones. Plan for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection. The key lies in phased implementation that validates core functionality before adding complex integrations.

Phase 1 (Q2-Q3 2025) focuses on core carrier connectivity. Start with your highest-volume carriers and most critical lanes. Build OAuth authentication, basic rate shopping, and label generation. Test these functions thoroughly before expanding scope. This foundation prevents the common mistake of building everything simultaneously and discovering fundamental architecture problems after significant investment.

Phase 2 (January 2026) aligns with regulatory readiness. As of January 2026, eFTI platforms and service providers can start preparing for operations, with Member States authorities potentially starting to accept data stored on certified eFTI platforms for inspection. Use this voluntary testing period for real-world validation of your compliance systems.

Phase 3 (July 2026) implements advanced features after regulatory requirements stabilize. This includes automated compliance reporting, cross-border documentation generation, and integration with emerging eFTI platforms. The phased approach prevents scope creep while ensuring regulatory deadlines don't compromise system quality.

Budget planning around these phases requires understanding both direct compliance costs and indirect operational impacts. European operations typically achieve measurable benefits once integrations stabilize. European operations often see 15-25% improvements in transport administrative efficiency within the first year of successful TMS data integration. These improvements come from reduced manual data entry, automated compliance reporting, and enhanced visibility across transport networks.

Vendor Selection Criteria That Actually Matter in 2026

Standard vendor scoring frameworks built around feature checklists miss the consolidation risks that now define procurement success. European regulatory expertise trumps generic functionality when compliance failures carry €5,000 fines per violation.

Evaluate vendors based on demonstrated European regulatory capabilities, not promises. Vendors claiming eFTI readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate. Platforms like Cargoson, Manhattan Active, MercuryGate, and Descartes each bring different approaches to ICS2 compliance, but European-native solutions often provide better understanding of cross-border complexity and multi-country regulatory variations.

The choice between European specialists and global mega-vendors involves trade-offs beyond functionality. Global platforms like Oracle TM and SAP TM provide enterprise integration advantages and broader functional scope but may deprioritize European-specific features during consolidation activities. The choice depends on organizational priorities between regional optimization and global standardization.

Financial stability assessment extends beyond traditional metrics during consolidation periods. Your vendor evaluation must now include financial stability assessment beyond traditional metrics. Financial health indicators become critical evaluation criteria in a consolidating market. European-focused vendors like Cargoson often provide acquisition resistance through regional focus, while global vendors face different consolidation pressures.

Test genuine API connectivity versus marketing promises during evaluation. Test integration capabilities with multiple carrier types simultaneously. Your chosen platform must connect seamlessly to road hauliers using different telematics systems, rail operators with varying data standards, and maritime carriers managing container tracking through diverse port systems.

Action Plan: 90-Day Migration Preparation Framework

The vendor consolidation timeline forces immediate action. Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as vendors focus resources on existing customer compliance rather than new client acquisition.

Days 1-30 require immediate vendor consolidation risk assessment. Evaluate your current TMS provider's acquisition vulnerability. Are they a target? Are they acquiring others? Document your critical carrier relationships, backup provider options, and spot market access requirements. Build contingency plans that include backup vendor qualification and contract termination scenarios.

Days 31-60 focus on regulatory compliance preparation. Use the January 2026 eFTI voluntary period strategically. Member States authorities may start accepting data stored on certified eFTI platforms for inspection from January 2026. Use this voluntary period for real-world testing and staff training. This testing window won't last forever, and early participants gain implementation experience before mandatory deadlines.

Days 61-90 represent your technology implementation window. Select your integration approach - build, buy, or hybrid - based on realistic assessment of internal capabilities and regulatory timelines. Cloud TMS implementations often conclude within eight weeks, compared to 6-18 months for traditional systems.

Contract protection strategies become essential during vendor consolidation. Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights. Standard TMS contracts don't address these scenarios, leaving shippers vulnerable to post-acquisition service degradation.

The mathematics are unforgiving, but they're not inevitable. European shippers who build systematic migration strategies around realistic cost planning, vendor stability assessment, and regulatory compliance timelines avoid the €50,000+ budget traps that derail reactive implementations. The question isn't whether to migrate - it's whether you'll control your integration costs or let them control your operations.